Broad economic and sector-specific tailwinds emerge across U.S. construction. The overall U.S. economy logged relatively strong +3.2% QoQ GDP growth in Q3-23, according to UBS. This is despite elevated interest rates and above target, but declining, inflation. Unemployment remains historically low and consumer spending robust.

ENR Industry Confidence Index is based on responses by U.S. executives of leading general contractors, subcontractors and design firms on ENR’s top lists to surveys

The commercial construction sector, which is sensitive to the performance of the economy, has benefited from these favorable demand dynamics. According to the Census Bureau, construction spending on healthcare properties is up +12.3% YoY, hotel spending is up +18.3% YoY, retail/wholesale property spending is up +4.4% YoY, and multifamily residential spending is up +24.5% YoY. While companies continue to evaluate their long-term office needs, spending on office properties is nevertheless up +9.3% YoY. Despite elevated interest rates and evolving owner preferences, commercial real estate valuations generally remain near pre-pandemic highs.

Resilient U.S. Economy Benefiting Residential and Industrial Sectors

The single-family residential sector is also benefiting from the resilience of the U.S. economy. While elevated mortgage rates have pressured affordability for buyers, the pace of rate increases in the underlying Federal Funds rate has slowed during 2023 as monthly inflation cooled. Meanwhile, the gap between U.S. household formation and required housing supply remains wide and existing for-sale inventories remain tight as would-be homesellers confront elevated mortgage rates.

Moreover, prospective buyers, reinforced with savings from the resilient economy, have turned to new construction to solve their housing needs. New single-family construction spending rose +6.7% QoQ (down -13.0% YoY) in Q3-23. Rising housing starts in Q2-23 and Q3-23 suggest that homebuilders anticipate stable demand, which could strengthen if inflation continues to decline and interest rates fall. The NAHB/Wells Fargo National HMI is up +0.7% QoQ/YoY in Q3-23.

In the industrial sector, demand tailwinds from the resilient U.S. economy have compounded with supportive government policies, particularly for manufacturing projects, and corporate reshoring trends. The IIJA, IRA, and CHIPS Act have provided tens of billions of dollars in direct funding and tax incentives for public and private manufacturing construction. Meanwhile, American companies like General Electric and Ford, are seeking to minimize geopolitical risk by rebuilding manufacturing capacity in the U.S. Manufacturing construction rose +65.9% YoY in Q3-23 and is +143.4% higher in Q3-23 compared to Q3-21. The civil sector has also benefited from supportive government policies, especially the IIJA.

After decades of underinvestment, the IIJA committed some $550B towards U.S. infrastructure construction over approximately ten years. According to a Q3-23 survey conducted by Procore and the AGC, 78% of civil contractors expected their backlogs to increase or remain the same in 2024. Major civil construction categories, including highways, streets, bridges, airports, railroads, and power stations, are generally about +10% YoY in spending in Q3-23.

West and Civil Construction Sectors Suggesting Future Market Growth

We anticipate that tailwinds will broadly benefit U.S. construction in the near term, but backlog data suggests particular strength in the West and in civil construction sectors. Continued cooling inflation, easing labor market tightness (but not large job losses), and stable-to-increasing demand will benefit construction stakeholders across segments. For example, the stabilization in construction materials prices after the surge in inflation in 2021 has eased friction in bidding and supported contractors’ margins across project types. Additionally, the ENR Confidence Index, which tracks U.S. GC and SC sentiment, is up +15.0% QoQ (+4.5% YoY).

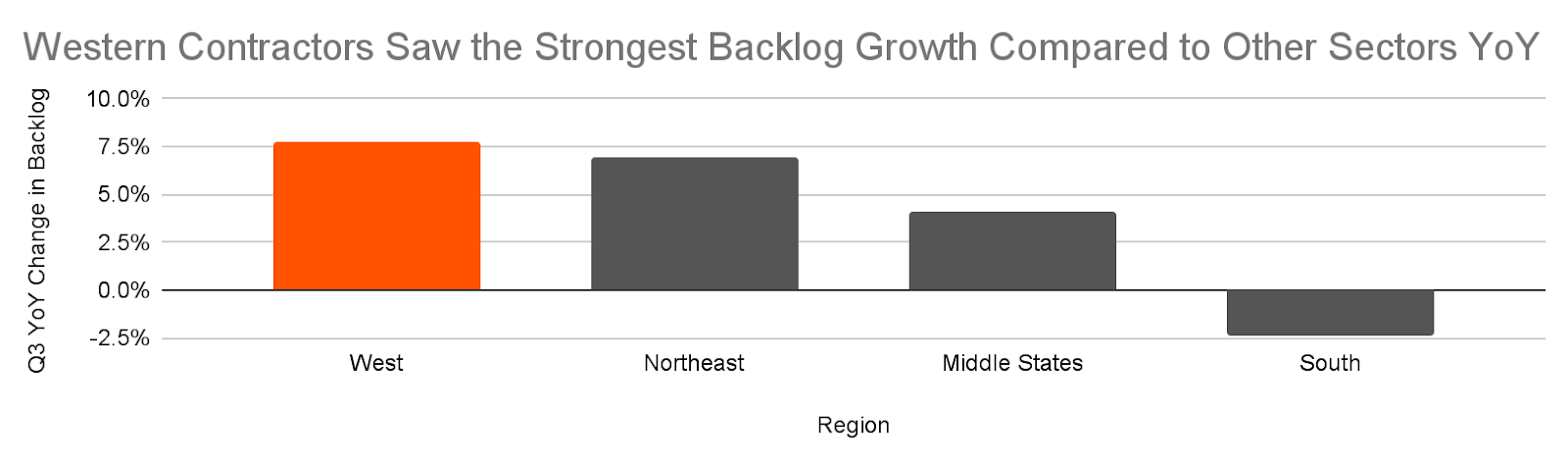

At the same time, some market segments’ outlooks reflect more significant exposure to tailwinds. Stakeholders located in the U.S. West appear well-positioned to benefit from U.S. economic resilience. Driven by the strong overall economic growth in the U.S. West, Western contractors reported to Associated Builders and Contractors (ABC) that their backlogs had grown more rapidly YoY compared to other regions. Lengthening backlogs suggest that Western contractors are experiencing demand in excess of their current capacity, suggesting future market growth.

Source: ABC Backlog Indicator

Meanwhile, the lengthening of civil contractors’ backlogs also suggests room for expansion in activity.

Source: ABC Backlog Indicator

To highlight the current tailwinds of the U.S. construction, Anirban Basu, chief economist of the ABC trade association, stated in September-23 that “there’s no sign of a construction recession in the near term. If anything, contractors are more upbeat, as policy and technology shifts along with economic transformation are creating substantial demand for improvements and growth in America’s built environment.”

Leave a Reply